Want to jump straight to the answer? The best forex broker for most people is definitely FOREX.com or IG.

Just about any forex trader who holds overnight positions past 5 p.m. NY time has had to deal with tomorrow/next (tom/next) rollovers. This activity typically occurs when a new trading day begins to make sure currency trading positions remain available for a type of delivery that takes place 2 business days from the transaction date (termed “value spot”) so traders can readily trade out of them in the spot market.

The pips charged or paid for doing those rollovers are determined using the principle of interest rate parity (IRP) that governs the relationship between forex forward rates and prevailing interest rates. Read on for more information about the forex forward market and how IRP underlies its quotations.

What Are Spot and Forward Rates?

In the forex market, currencies trade in pairs at a particular rate of exchange or “exchange rate” for immediate delivery as soon as is practically possible.

For most currency pairs, that immediate delivery date is known as “value spot,” which is derived from the phrase “on the spot” and lies 2 business days in the future from the trade date. A few popular pairs, like USD/CAD, frequently trade for value “tomorrow,” “tom,” or “funds,” which are 1 business day from the trade date.

In contrast to spot rates, forward outright rates or simply “forward rates” are exchange rates for a currency pair for any value date that is not the normal spot or funds value date for that particular pair.

In the Interbank forex market, forward outright transactions can be quoted on and executed for virtually any future delivery date. Furthermore, forward quotes for the standard time periods or “tenors” of duration, including overnight; tomorrow; 1, 2, and 3 weeks; 1 through 11 months; and 1 through 5 years, are also generally available.

The equation for calculating forex forward outright rates using the U.S. dollar as the base currency from the spot rate and prevailing interest rates in the foreign and domestic countries is:

Forward Rate = Spot Rate * (1+IRF)/(1+IRD)

Where:

IRF = The interest rate for the foreign country

IRD = The interest rate for the domestic country (USD in this case)

Forward Swap Points Explained

Swap points are the difference in pips between the spot rate (or the funds rate for pairs like USD/CAD) and the forward outright rate corresponding to a particular delivery date. Swap points can be positive or negative, depending on the interest rate differential between the pair of currencies.

The swap points quoted in pips for outright forwards and for rolling a forex position out to any forward delivery date can be computed from and depend in a precise way (thanks to IRP) on the interest rate differential between the 2 currencies involved.

To calculate swap points, you’ll require both the spot exchange rate and the 2 currencies’ interest rates for the forward value date the position is being rolled or “swapped” out to. Interbank deposit or “depo” rates are usually used for this purpose.

For currency pairs like USD/JPY or USD/CAD with the U.S. dollar as the base currency, you can compute swap points using this equation:

Swap points = Forward Rate-Spot Rate = Spot Rate *[(1+IRF)/(1+IRD)-1 ]

Where IRF and IRD remain as defined in the previous section.

Note that if the foreign interest rate is higher than the domestic interest rate for a particular forward delivery date, then the corresponding forward swap points will be positive. This circumstance is known as “trading at a forward premium,” and it means you pay a higher outright exchange rate for the currency pair for delivery on that forward date versus delivery on the nearer spot date.

If the opposite situation arises, then the swap points will be negative. Known as “trading at a forward discount,” in this case you pay a lower exchange rate for a forward outright trade than for a spot trade.

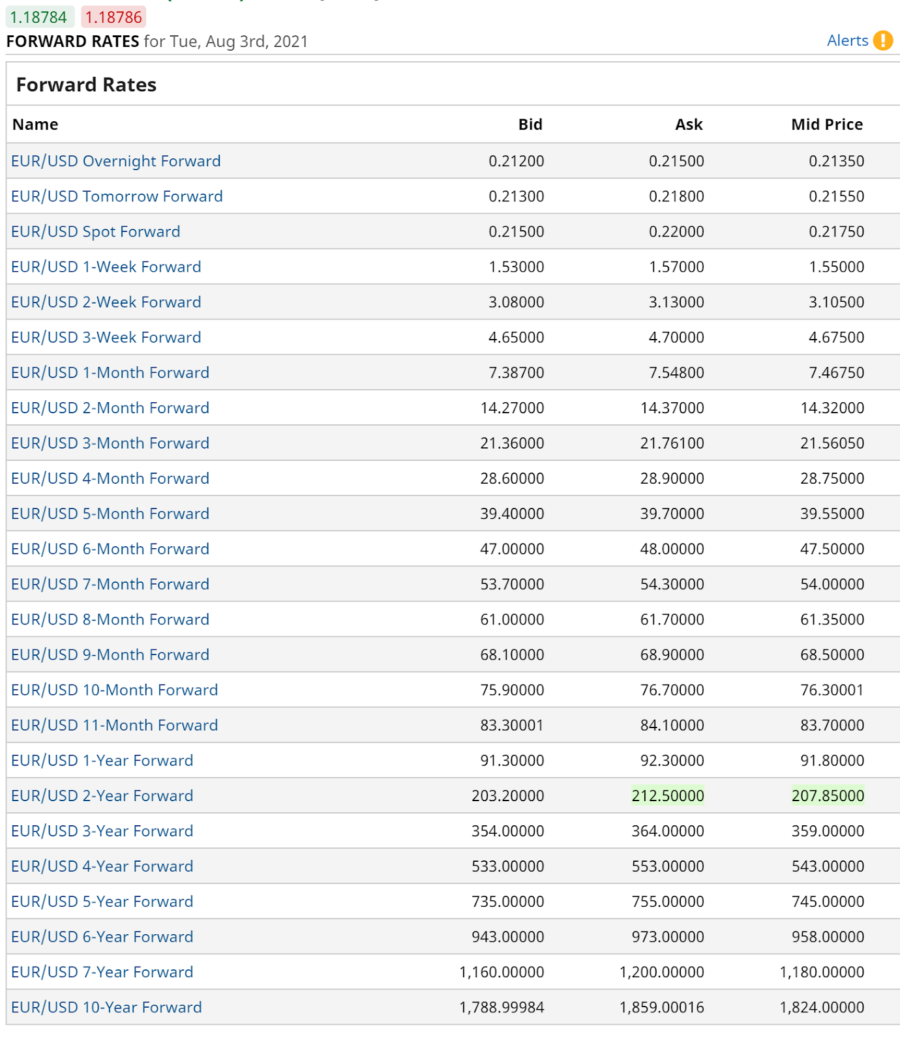

The table below displays swap points for the EUR/USD currency pair for a series of forward delivery dates. Note that the offered spot rate for EUR/USD appears in red at the top as 1.18786. Also, the offer side swap points for a 1-month EUR/USD forward are 7.548 pips or 0.0007548, since each pip in EUR/USD corresponds to 0.0001 in the exchange rate. Using that information, the indicative quote a forex dealer might show its client for the offer side on 1 month forward outright rate for EUR/USD would be 1.18786+0.0007548 = 1.1886148.

Swap points in pips for standard forward outright tenors for EUR/USD. Source: BarChart.com.

What is IRP?

The basic premise of IRP is that hedged returns from making deposits in different currencies should be identical, no matter what interest rates they pay. A possible sequence of transactions that might take place in an arbitrage transaction based on IRP could include the following:

- Borrow the currency with the lower interest rate.

- Convert the borrowed money into the higher interest rate currency using a spot transaction.

- Invest the higher interest rate currency proceeds into an interest-bearing asset from its native country.

- Buy the lower interest rate currency against the higher interest rate currency using a forward outright contract for delivery when the interest-bearing asset matures.

Unfortunately for the retail trader, any significant deviations from IRP are quickly removed by astute professional traders engaged in arbitrage at major financial institutions. Arbitrage involves the simultaneous buying and selling of a similar asset in different markets for a locked-in profit.

Furthermore, “Covered Interest Rate Parity” (CIP) refers to an equilibrium situation in the relationship between spot, forward and interest rate markets when no opportunity for forward contract/interest rate arbitrage is available. In this ideal situation, forward cover rates for forex risk allow for no net profit given prevailing deposit interest rates.

In contrast, the theory of “Uncovered Interest Rate Parity” (UIP) states that the interest rate differential between 2 countries should equal the relative exchange rate shift among their national currencies over a given period. UIP implies that the return expected from a domestic asset will equal that of a similar foreign asset after you adjust for forex rate changes.

The UIP theory can be used by academic economists and market analysts to forecast future foreign exchange rates, although the limited evidence supporting it suggests it represents little more than an educated guess of what rational expectations for future foreign exchange rates should be.

IRP Arbitrage Requires More Than Research

If you want to engage in IRP arbitrage, you must do your research and understand the math involved so that you have a good idea of when interest rates and forex forward rates are sufficiently out of alignment to create opportunities.

Keep in mind that arbitrage to exploit temporary misalignments between the interest rate and forex forward markets is typically performed by professional traders working at major money center banks. They can sometimes do this profitably since they have access to the best market pricing for deposits and swaps.

There may therefore be rather slim pickings left for smaller arbitrageurs, so for retail forex traders working within a modest margin account, this sort of activity might not make sense. They might be especially disadvantaged since they usually have slower pricing feeds, reduced reaction times and wider dealing spreads to cross.

Also, if their broker does not let them perform such arbitrage at reduced margin rates, then retail forex traders might have to tie up substantial amounts of margin for what is typically a very small net gain, albeit a largely risk-free one.

Benzinga’s Best Forex Brokers

If you are considering starting to trade forex for your personal account, then you will probably need a margin account at an online forex broker. Benzinga has taken the guesswork out of this process by compiling the list below of the best forex brokers currently available.

Is IRP Arbitrage Suitable for you?

If you do intend to attempt this sort of trading activity, you will probably be a more analytical trader who prefers to watch for opportunities to lock in gains while taking minimal risk.

In any case, you will need to trade through 1 or more reputable financial institutions that allow you to trade outright forex forward contracts and either make deposits or invest in other interest-bearing investments in foreign countries as efficiently as possible.

Frequently Asked Questions

What is the CIP formula?

The CIP formula describes an equilibrium situation in the relationship between the spot, forward and interest rate markets when no opportunity for forward contract/interest rate arbitrage is available.

What is CIP?

IRP posits that returns from making deposits in different currencies should be identical when hedged with a forward outright contract, no matter what interest rates each currency pays. CIP describes the equilibrium situation when arbitrage opportunities are not available among the deposit and forex forward markets.

FOREX.com, registered with the Commodity Futures Trading Commission (CFTC), lets you trade a wide range of forex markets plus spot metals with low pricing and fast, quality execution on every trade.

ForexSignals.com offers a highly rated platform with mentors who have 80 years of combined experience in the trading pits. They’ll help you decode real-time daily live streams using market analysis, trade signals and more. ForexSignals.com doesn’t stop there. You can access hundreds of educational videos and workshops and even individualized private sessions with mentors. Never trade alone! Join ForexSignals.com now.

https://www.benzinga.com/money/interest-rate-parity-for-forex-traders/

2021-08-03 17:59:18Z

CBMiRmh0dHBzOi8vd3d3LmJlbnppbmdhLmNvbS9tb25leS9pbnRlcmVzdC1yYXRlLXBhcml0eS1mb3ItZm9yZXgtdHJhZGVycy_SAQA

Bagikan Berita Ini

0 Response to "Interest Rate Parity for Forex Traders • Cover Rate Forex • Benzinga - Benzinga"

Post a Comment