Scott Olson

Introduction

Today, Apple's (NASDAQ:AAPL) stock is nearing its historical highs despite worries about worsening macroeconomic conditions. Inflation, although starting to cool down, continues to be above the Federal Reserve's target rate prompting the Federal Reserve to continue its rate hikes while the signs of macroeconomic weaknesses such as the current volatility shown in the banking sector persist. As such, some investors worry that Apple stock may be expensive. However, I believe otherwise. Forex environment, for Apple, is becoming more favorable reducing the headwinds facing the company, and despite popular belief, I continue to see Apple's version of innovation pushing consumer preference and demand forward, and these combinations, in my opinion, will keep the rally afloat as the consumer demand for smartphone and discretionary goods return toward the end of 2023 or starting in 2024. Therefore, I believe the current stock rally is sustainable, and believe that Apple is a buy.

Forex Market

In the most recent earnings call, Apple's management team made it clear that the US Dollar's strength has created a headwind for them as they have said that "the foreign exchange will continue to be a headwind, and we expect a negative year-over-year impact of 5 percentage points." This comment was made on February 2nd; however, today, the foreign exchange environment has radically shifted as global investors questioned the longevity of the US Federal Reserve's intent to raise rates.

The US banks started to show signs of weakness which resulted in the US Treasury Department and the Federal Reserve taking prompt actions. The joint statement by the Department of the Treasury, Federal Reserve, and the FDIC, states that the government "is taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system" by "protecting deposits and providing access to credit." The government's intervention signals to investors the potential limitations to raising rates even after the Federal Reserve President Jerome Powell signaled to Congress a strong intent to fight inflation days before the Silicon Valley Bank's failure. Therefore, with global investors weighing the likelihood of the Federal Reserve finishing its rate hike in the near future, the US Dollar has started to decline relative to foreign countries.

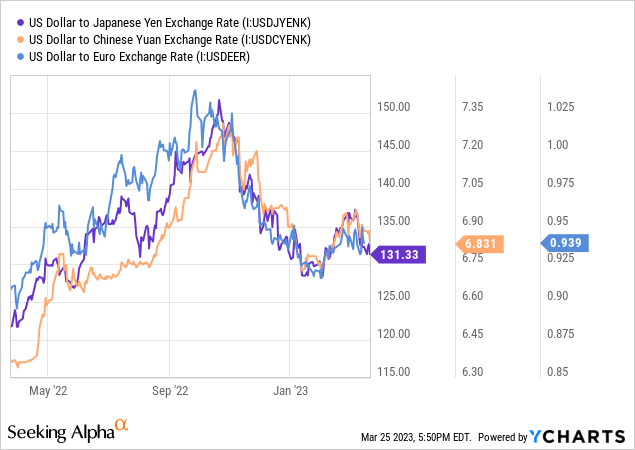

As the charts above show, the value of the US dollar is continuing its downward trajectory, which will likely offset the headwinds faced by Apple in a significant way. In reaction to rising rates in 2022, Apple significantly raised the price of its products in global markets except for the United States and China; thus, as the exchange rate normalizes, I believe that Apple will see outsized gains from its price hikes made in 2022.

Japan, the U.K., Germany, and more global markets saw a price hike for iPhone 14 in 2022. The price of a standard iPhone increased by 21,000 Yen or 21.3% in Japan, 70 pounds or 9% in the U.K., and 100 Euros or 11.1% in Germany. As such, because these moves were made due to the strengthening of the US dollar, as the dollar's strength weakens, Apple is expected to benefit from both the price hike and the favorable exchange rate. Therefore, as the dollar starts to weaken relative to other currencies, Apple is expected to reap the benefits.

Innovation is Still Here

Many investors point out that Apple's innovation has stopped because, on the surface level, it seems as if Apple is releasing the same product over and over again with minor changes. If this is to be true, it should be regarded as a significant risk as a technology company with lacking innovation will quickly fall behind its competitors. However, I believe Apple's innovation has never stopped. In fact, I continue to see massive innovation happening all around Apple as Apple's innovation is not defined by pouncing on all of the newest technologies. Instead, Apple's innovation comes from perfecting the newest technologies before releasing them even if this allows the competitor to claim the first to market. I view this to be a critical advantage that Apple has.

Looking at Apple's previous product launches, I believe my claim is reasonable. Apple was never the first to market, but its product, when it was released, was regarded as one of the best due to Apple's unique approach to innovation. For example, Apple did not invent the first smartphone, wireless earbuds, laptops, smartwatches, music streaming services, and tablets, yet the company's unique branding, marketing, and quality have allowed Apple to arguably win in the market. Even in recent years, Apple's version of innovation continued. There were plenty of competitors with light laptops, but Apple perfected it by removing a fan in 2020 while maintaining its performance. As such, I do not think it is fair to say Apple is not innovative today as the company's innovation continued in its own unique ways.

I believe these aspects of Apple create the company's loyal demand. I do not think the majority of consumers want the newest tech; instead, I think that they want new technologies that work well, which is the reason why I believe that Apple's customers tend to be loyal and the market preference for Apple continues to grow. Not only did iPhone see its largest global market share of all time in 2022Q4, but according to the Wall Street Journal, "consumers around the world are increasingly choosing Apple Inc.'s iPhones over high-end Android smartphones." This claim is backed by a poll that "show[s] that people in their teens and early 20s" are "increasing[ly] [seeing] the iPhone as a must-have." Therefore, it may be wrong to say that Apple's innovation has stopped as the company continues its own version of innovation gradually growing the products' preference.

Demand Environment

Although the global smartphone market is expected to decline by 1.1% in 2023, market growth is expected to start picking up in 2024 with a 5.9% growth. Given that the forex headwinds are potentially turning into tailwinds while Apple's version of innovation is continuing to drive market share and preference for the company's products, I believe the company will be back on its growth trajectory as the overall consumer demand environment improves.

Risk to Thesis

Despite my bullish view of Apple, the macroeconomic conditions pose risks to my bullish thesis. With cracks in the financial world starting to show with Silicon Valley Bank, First Republic (FRC), Credit Suisse (CS), and potentially Deutsche Bank (DB), global economic conditions may quickly deteriorate causing a recession. In such a scenario, my bullish thesis may be challenged as consumers and corporations alike will cut discretionary spending.

Summary

Apple's recent bullish run is likely to continue. Going into 2023, the company forecasted continued forex headwinds; however, with a recent turnaround of events in the banking sector causing a weakness in the US dollar, the potential headwind from the forex rates will likely turn into a headwind due to Apple's pricing increase in global markets in 2022. Further, with Apple's continued innovation leading to customer preference and market share, I believe Apple is in a prime position to return to a growth trajectory as consumer demand for smartphones returns toward the end of 2023 or starts in 2024. Therefore, I continue to believe that Apple is a buy.

https://news.google.com/rss/articles/CBMiX2h0dHBzOi8vc2Vla2luZ2FscGhhLmNvbS9hcnRpY2xlLzQ1OTAxOTctYXBwbGVzLXJhbGx5LWxpa2VseS1zdXN0YWluYWJsZS1mdWVsZC1mb3JleC1pbm5vdmF0aW9u0gEA?oc=5

2023-03-26 14:02:35Z

CBMiX2h0dHBzOi8vc2Vla2luZ2FscGhhLmNvbS9hcnRpY2xlLzQ1OTAxOTctYXBwbGVzLXJhbGx5LWxpa2VseS1zdXN0YWluYWJsZS1mdWVsZC1mb3JleC1pbm5vdmF0aW9u0gEA

Bagikan Berita Ini

0 Response to "Apple's Rally Is Likely Sustainable Fueled By Forex And Innovation (NASDAQ:AAPL) - Seeking Alpha"

Post a Comment