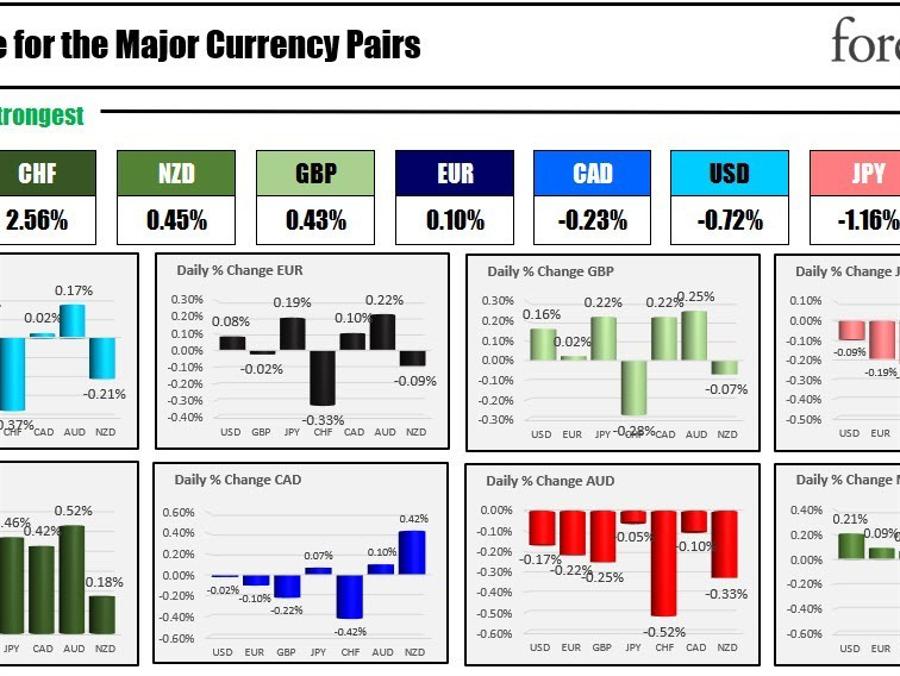

The strongest to the weakest of the major currencies

The CHF is the strongest and the AUD is the weakest as the North American day (and week gets started). For today, U.S. President Joe Biden and House Speaker Kevin McCarthy are scheduled to meet to negotiate an agreement to raise the U.S. debt ceiling, aiming to avoid a potentially damaging default. McCarthy and Biden spoke on Sunday as Biden made his way back from the G7 summit in Japan and the conversations were constructive/positive. The leaders are working toward the June 1 deadline where money is set to run out. Stock futures are steady as traders are reluctant to move either way as the talks are set to continue. In other weekend news, China banned its local infrastructure operators from purchasing chips from U.S. semiconductor giant Micron, causing its share prices to drop. Each country are moving away from each other as concerns about security prevail. The decision also came as G7 leaders criticized Beijing's trade practices during a summit in Japan. Additionally, oil prices fluctuated due to the uncertainty surrounding the U.S. debt ceiling negotiations (currently up modestly). Traders today will also be focused on Fed Speak with Fed's Bullard (8:30 AM ET), Barkins (10:50 AM ET), and Daly (11:00 AM ET) all scheduled to speak. Minneapolis Federal Reserve President Neel Kashkari said this morning that the current banking stress isn't helping mitigate inflation, suggesting that the Fed needs to persist in its efforts to curb inflation. He pointed out that the inflation of services seems to be significantly entrenched, hinting at the complexity of the issue. Kashkari also suggested that it may be necessary to push interest rates above 6% to combat inflation, although the need for such a significant increase remains uncertain.

Today - other than the Fed speak - is void of economic releases. Canada is on holiday in observance of Victoria Day. The week has some key events however.

On Tuesday, May 23rd, France, Germany, the Eurozone, and the US all released their May flash manufacturing, services, and composite PMI data. The releases provide key insights into the current economic climate in these regions and are closely watched by investors worldwide.

On Wednesday, May 24th, New Zealand releases its Q1 retail sales data, providing a look into consumer spending trends at the start of the year. On the same day, the Reserve Bank of New Zealand (RBNZ) made its monetary policy decision (+25 basis points), which is of significant interest given its impact on interest rates, inflation, and overall economic stability. In the UK, April's Consumer Price Index (CPI) figures will be released, offering insights into inflation trends. Germany unveils its May Ifo business climate index, providing a gauge of business optimism and economic direction in the country. The day also witnesses US Treasury Secretary Yellen speaking on the economy, shedding light on the administration's perspective on current economic conditions and future policy directions. The Federal Open Market Committee (FOMC) releases its May meeting minutes, giving markets an insight into the Federal Reserve's monetary policy deliberations.

The focus shifts to the US again on Thursday, May 25th, with the release of weekly initial jobless claims, which provide a measure of the health of the labor market, and the second estimate of Q1 GDP (est 1.1%), offering a more refined view of economic growth in the first quarter.

Friday, May 26th, will bring the release of the UK's April retail sales data, providing another perspective on consumer spending in the country. Lastly, the US reported its April durable goods orders, an important indicator of demand for longer-lasting goods and an insightful economic health marker. These releases, collectively, offer a comprehensive picture of the current state of various global economies and the potential economic trends in the near future.

A snapshot of the markets are showing:

- WTI crude oil is up $0.09 or 0.11% at $71.77

- Gold is down $4 or -0.20% at $1973.18

- Silver is down $0.07 or 0.32% at $23.77

- Bitcoin trades steady versus Friday at $26,845. The low price today reach $26,547 which tested its rising 100 day moving average at $26,536

In the premarket for US stocks, the major indices or higher after Friday's modest declines:

- Dow Industrial Average is up 36.37 points after Friday's -109.28 point decline

- S&P is up 4 points after Friday's -6.07 point decline

- NASDAQ index is up 8 points after Friday's -30.94 point decline

In the European equity markets, the German DAX is correcting from its all-time high close on Friday

- German DAX -0.35%

- Frances CAC -0.29%

- UK's FTSE 100 +0.6%

- Spain's Ibex +0.54%

- Italy's FTSE MIB -0.73%

In the US debt market yields are modestly lower:

- 2 year yield 4.268% -2.1 basis points

- 5 year yield 3.732% -1.4 basis points

- 10 year yield 3.684% -0.8 basis points

- 30 year yield 3.944% -0.3 basis points

In the European debt market, yields are higher in the benchmark 10 year sector:

European 10 year yields

https://news.google.com/rss/articles/CBMijwFodHRwczovL3d3dy5mb3JleGxpdmUuY29tL3RlY2huaWNhbC1hbmFseXNpcy90aGUtY2hmLWlzLXRoZS1zdHJvbmdlc3QtYW5kLXRoZS1hdWQtaXMtdGhlLXdlYWtlc3QtYXMtdGhlLW5vcnRoLWFtZXJpY2FuLXNlc3Npb24tYmVnaW5zLTIwMjMwNTIyL9IBkwFodHRwczovL3d3dy5mb3JleGxpdmUuY29tL3RlY2huaWNhbC1hbmFseXNpcy90aGUtY2hmLWlzLXRoZS1zdHJvbmdlc3QtYW5kLXRoZS1hdWQtaXMtdGhlLXdlYWtlc3QtYXMtdGhlLW5vcnRoLWFtZXJpY2FuLXNlc3Npb24tYmVnaW5zLTIwMjMwNTIyL2FtcC8?oc=5

2023-05-22 12:14:00Z

CBMijwFodHRwczovL3d3dy5mb3JleGxpdmUuY29tL3RlY2huaWNhbC1hbmFseXNpcy90aGUtY2hmLWlzLXRoZS1zdHJvbmdlc3QtYW5kLXRoZS1hdWQtaXMtdGhlLXdlYWtlc3QtYXMtdGhlLW5vcnRoLWFtZXJpY2FuLXNlc3Npb24tYmVnaW5zLTIwMjMwNTIyL9IBkwFodHRwczovL3d3dy5mb3JleGxpdmUuY29tL3RlY2huaWNhbC1hbmFseXNpcy90aGUtY2hmLWlzLXRoZS1zdHJvbmdlc3QtYW5kLXRoZS1hdWQtaXMtdGhlLXdlYWtlc3QtYXMtdGhlLW5vcnRoLWFtZXJpY2FuLXNlc3Npb24tYmVnaW5zLTIwMjMwNTIyL2FtcC8

Bagikan Berita Ini

0 Response to "The CHF is the strongest and the AUD is the weakest as the North American session begins - ForexLive"

Post a Comment